Research

Choose Language

November 8, 2024

Weekly InsightsWeekly Investment Insights

Last week, the result of the US Presidential election was finally announced, with Donald Trump elected as the President of the United States for the second time. Even before all the votes were counted, bitcoin and US bond yields jumped, and the dollar surged as investors placed their bets on Trump. In Europe, renewable companies slumped, the euro fell against the dollar and government bond yields dove in anticipation of Trump’s promised trade tariffs.

US stocks soared to record highs in anticipation of lower corporate taxes and looser regulation. The S&P 500 index climbed to its best day in two years and the Russell 2000 index of small-cap companies jumped after Trump's victory, outperforming broader market indices such as the S&P 500 and the Dow Jones Industrial Average.

The aggressive trade tariffs proposed by President Trump and the inflationary environment that could result from them caused investors to sell bonds, pushing fixed income yields sharply higher.

Weekly roundup

The US Fed & Bank of England cut interest rates by 25 basis points

The Fed lowered its key rate by 25 basis points last week, bringing the policy rate to 4.50% - 4.75%. Fed Chairman Jerome Powell reiterated the Fed's focus on its dual mandate of maximum employment and stable prices. He noted that the unemployment rate has moved up but remains low, and that inflation has made progress toward the committee's 2% objective but remains somewhat elevated. He also said “that economic activity has continued to expand at a solid pace. GDP rose at an annual rate of 2.8 percent in the third quarter, about the same pace as in the second quarter. Growth of consumer spending has remained resilient, and investment in equipment and intangibles has strengthened.”

Turning to the labour market, Powell observed that job gains had slowed from earlier in the year, but that labour strikes and hurricanes had had an impact. Overall, labour market conditions were described as solid.

Regarding future rate cuts, Powell reiterated that the Fed's path has not yet been decided and that it will continue to decide on a meeting-by-meeting basis.

The decision to cut rates comes just two days after the presidential election, which Powell said would have no "near-term" impact on monetary policy. The Fed will need to continue to monitor developments in the labour market and inflation to determine its next steps.

While the Fed is expected to lower rates further in the coming months, investors and economists have pared back expectations for how low rates will fall this cutting cycle, partly in response to Trump’s election.

On the other side of the Atlantic, the Bank of England (BoE) decided last week to cut interest rates by 25bp for the second time this year, bringing the Bank Rate down to 4.75%. The decision was widely expected after inflation fell below the BoE's 2% target to 1.7% in September. Although underlying inflationary pressures have eased, the central bank expects inflation to pick up following the announcement of the Autumn Budget, which the BoE believes will add just under half a percentage point to the inflation rate at its peak.

"We need to make sure inflation stays close to target, so we can't cut interest rates too quickly or by too much," BoE Governor Andrew Bailey said.

Investors also expect President Trump's proposed trade tariffs to contribute to rising inflation in the UK.

In terms of growth, the BoE expects the budget to increase the size of the UK economy by around 0.75% next year.

The US dollar surged on Trump’s election victory news

As the final votes were being counted in the US presidential election last week, investors betting on a Trump victory pushed the dollar to the strongest level in a year. The high trade tariffs promised by Trump risk boosting inflation, which in turn could force the Fed to slow the pace of interest rate cuts. If this happens, the dollar could strengthen further as higher interest rates increase the appeal of the currency.

However, a strong dollar could also hurt US companies that rely heavily on exports, making their products more expensive for customers around the world. President Trump's promised tariffs could also cause US trading partners to implement tariffs of their own.

In any case, the tariffs are likely to have a major impact on the direction of the dollar. It remains to be seen, however, when and how the tariffs will be implemented.

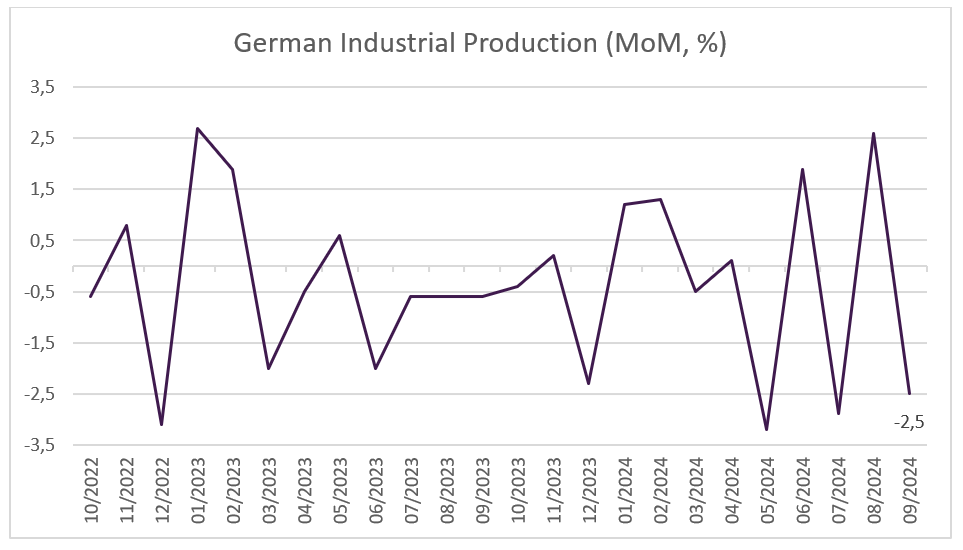

German factory orders pick up but industrial production falls

German factory orders rose by 4.2% in September compared with the previous month, beating market expectations. The increase was driven by large orders for aircraft, ships and trains, as well as a slight rise in new orders for automobiles. Total foreign orders rose by 4.4%, with Eurozone new orders rising by a notable 14.6%. Orders from the rest of the world, however, fell by 1.6%.

While this is a positive sign, the election of Trump and his promised trade tariffs are likely to weigh heavily on German industry going forward. Germany's trade surplus fell to €17bn in September from €21.4bn in August, with exports down 1.7% on the month. If President Trump's trade tariffs are implemented as promised, this could further depress exports in the coming quarters, as 10% of German exports go to the US.

Industrial production also fell, from a 2.6% rise in August to a 2.5% fall in September. Most sectors continue to struggle, but the car industry is particularly hard hit. This suggests that German industry is not yet fully on the road to recovery, despite the rise in factory orders.

Source: Bloomberg, BIL

China announces more support

Following Beijing's monetary stimulus package in September, a debt swap package was announced on Friday. The package aims to ease the debt repayment burden on local governments by allocating 10 trillion yuan ($1.40 trillion) to reduce off-balance sheet debt. Chinese Finance Minister Lan Foan has also signalled that more fiscal stimulus is on the way. So far, the announced stimulus has lacked support to boost weak consumer demand, which investors have been eagerly awaiting.

The Chinese economy has struggled with a property crisis, deflationary pressures and weak demand this year, and Trump's threat of 60% tariffs on all Chinese goods is likely to add to the pressure.

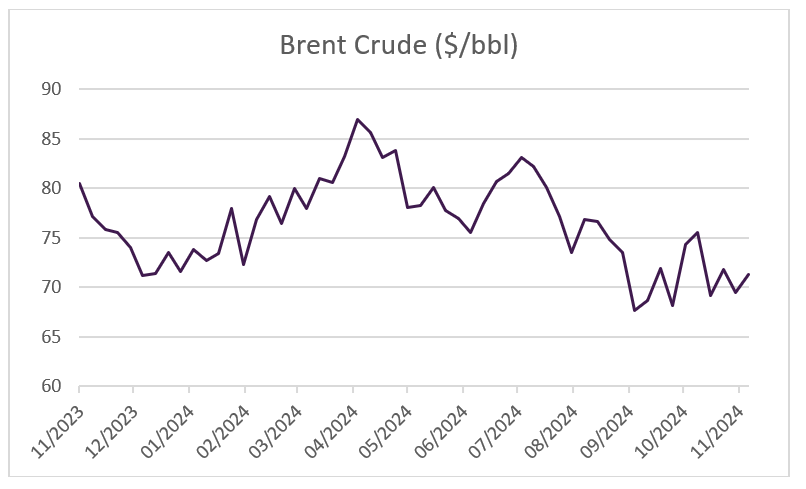

Opec+ members delay planned oil production increase

In a further attempt to revive oil prices, Opec+ announced last week that it would keep all production cuts in place until the end of the year. Over the past year, Brent crude has fallen by almost 14% amid weak global demand, particularly from the world's largest oil importer, China. Prices have risen on several occasions over the past year in response to growing fears that an escalation in the Middle East conflict could disrupt supply. However, weak demand has so far proved to be persistent.

Source: Bloomberg, BIL, As at 11am 08/11/24

Economic calendar for the week ahead

Monday – Bank of Japan Summary of Opinions.

Tuesday – Eurozone & Germany ZEW Economic Sentiment Index (November). Germany Inflation Rate (Final, October). UK Unemployment Rate (September). US Consumer Inflation Expectations (October).

Wednesday – US Inflation Rate (October).

Thursday – UK GDP Growth Rate (Prel, Q3), Balance of Trade (September), Industrial Production (September), Manufacturing Production (September). Eurozone Employment Change (Prel, Q3). US Jobless Claims, PPI (October).

Friday – Japan GDP Growth Rate (Prel, Q3). US Retail Sales (October), Industrial Production (October), Manufacturing Production (October).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

March 10, 2025

NewsInvestors begin to get back their app...

Written as at 6th March 2025 European equites have taken centre stage in 2025, defying expectations and outpacing their US counterparts. The Europe Stoxx 600...

March 3, 2025

Weekly InsightsWeekly Investment Insights

Volatility on global equity markets continued last week amidst various announcements from the Trump administration, big tech earnings and a mixed bag of economic...

February 24, 2025

Weekly InsightsWeekly Investment Insights

German stocks started the week with a boost as investors welcomed the conservatives’ victory in the national elections. The hope now is that the...

February 24, 2025

BILBoardBILBoard February 2025 – Repainting t...

When President Trump took office on January 20th, it was clear that tackling the US trade deficit would be a high priority. This is not...

February 17, 2025

Weekly InsightsWeekly Investment Insights

Stocks on both sides of the Atlantic finished higher last week. Stateside, the S&P 500 Index and Nasdaq Composite both closed the week within 1%...