Research

Choose Language

November 18, 2024

Weekly InsightsWeekly Investment Insights

Less than two weeks after the US Presidential election, Trump has made significant progress in nominations for top government posts, leading to some market volatility. The Republicans have defeated the Democrats in the race for a majority in the House of Representatives, making this election a red sweep and giving Trump more power to push his agenda through. In the US and beyond, companies and governments are now gearing up for the start of a second Trump presidency starting January 20th.

Market focus shifted last week as investors turned to inflation for clues on the pace of Fed rate cuts. October’s slight inflation uptick, while in line with expectations, is perturbing markets given that it occurs even before Trump comes into office. A continuation of this trend could impede on the path to lower Fed interest rates in 2025. Global equities fell and US Treasury yields rose sharply in anticipation of Trump’s inflationary policies, a reality that becomes more likely following his recent nominations.

While Trump was being confirmed as the winner of the US Presidential election, here on European soil, Germany’s “traffic light” coalition was collapsing. With the German economy facing a storm of structural and cyclical headwinds, a period of political uncertainty could push things from bad to worse, with businesses postponing decision-making and investment further. Both Germany and the wider Eurozone face a stuttering economic recovery and the time for a policy vacuum is hardly optimal. Despite this outlook, German stocks lit up on the announcement, with the DAX outperforming European peers on the prospect of a new government with enhanced decision-making power.

Gold had its worst week in three years and Brent crude fell to around $71 a barrel. In Europe, natural gas prices hit a YTD high after Russia announced that it would halt supplies to Austria. Cold weather, which arrived earlier than usual in some parts of Europe, has further highlighted the resulting supply concerns.

This week, all eyes are on Nvidia’s earnings results which could provide the market’s net major catalyst – for better or for worse. Traders will be watching for guidance about demand for Blackwell AI chips.

Weekly roundup

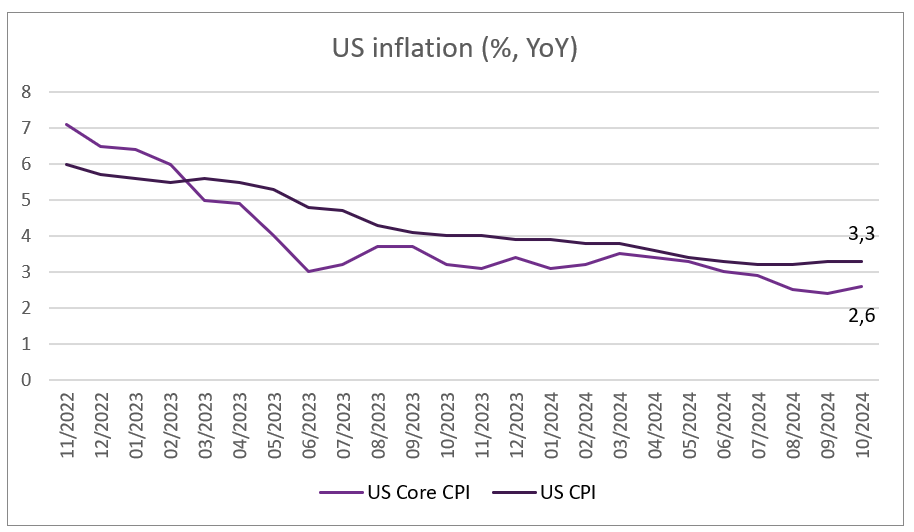

US inflation and retail sales rose in October

The inflation rate in the US rose to 2.6% YoY in October, from 2.4% in September. It marks the first increase in consumer prices in seven months.

The bulk of the rise was largely due to the shelter component. On a monthly basis, CPI rose by 0.2%, with the shelter index rising by 0.4%, accounting for more than half of the monthly increase.

Core inflation, which excludes items like food and energy, remained steady at 3.3%.

Source: Bloomberg, BIL

The decline in energy and fuel costs slowed, while gas prices rose. Price increases for food and transport slowed. Services inflation remained elevated at 4.7% YoY.

Also in October, retail sales rose by 0.4%, beating market expectations of a 0.3% rise. Households spent more at car dealerships, on electronic goods and on eating and drinking out. Sales of building materials, garden equipment and online retailers also rose, while sales at clothing stores fell. Fed Chair Jerome Powell said last week that "the economy is not sending any signals that we need to be in a hurry to lower rates." The relatively upbeat sales report reflects this sentiment, suggesting that the US consumer will continue to drive economic growth in the final quarter of the year.

The inflation print, along with robust retail sales data, leaves markets on the fence as to whether the Fed will cut rates again in December. Another concern for the outlook of Fed’s rate cuts is the inflationary aspects of Trump's proposed policies, which could change the direction of inflation in the longer term and lead the Fed to change the path of its monetary easing next year.

Uncertainty in Germany causes economic sentiment to dwindle

2024 has been a challenging year for the German economy. President-elect Donald Trump's tough trade stance and the collapse of Germany's coalition government have not improved the outlook for the eurozone's largest economy.

Since November 2023, the German government has struggled to address a multi-billion gap in its 2025 budget following a Constitutional Court ruling against using unspent pandemic funds for additional defense and climate spending. Chancellor Olaf Scholz and Finance Minister Christian Lindner have been unable to reconcile their differences over debt-financed spending to support Ukraine. Scholz wanted to raise the debt level, while Lindner argued it would violate his oath of office. Tensions escalated on the day of the US Presidential election when Scholz fired Lindner.

The President must now call an early election, but not before a no confidence vote has taken place. The timeline of this is still uncertain, raising concerns that Germany may not have a new government before June next year.

The German economy is facing somewhat of an existential crisis. It no longer has a steady supply of cheap energy, competition from China is intensifying and its industrial sector is under immense pressure. Productivity is low and an infrastructure update is long past overdue.

Decisive action needs to be taken, some economists purport this will also entail a review of the “Schwarze Null” debt brake - a requirement for balanced budgets enshrined in the German Constitution since 2009. This rule has kept Germany’s fiscal standing strong, with a debt-to-GDP ratio of 62%. However, economists argue that to remain competitive, Germany must loosen up the purse strings and start investing in its future.

Amid this uncertainty, economic sentiment in Germany has weakened, dropping from 13.1 in October to 7.4 in November, heavily influenced by Trump's victory and the coalition government's collapse.

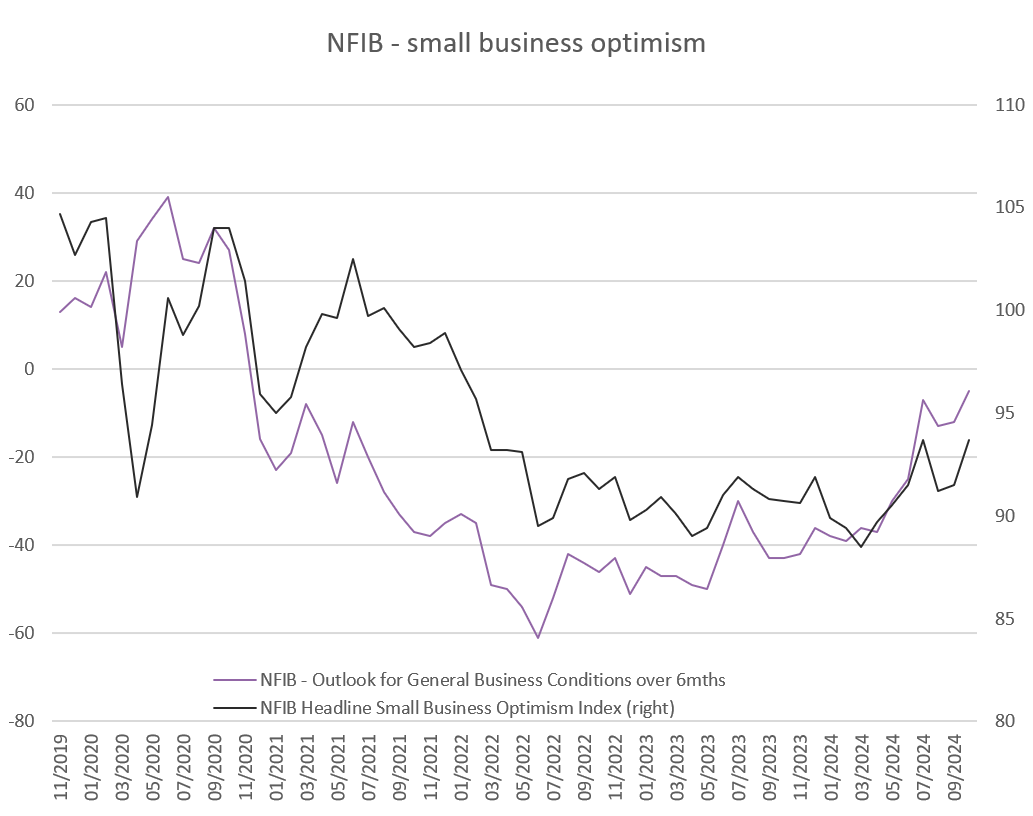

Small business optimism picks up – thank Trump

Last week, the NFIB survey showed optimism among small businesses rising to the joint-highest level since 2022. Main street American tend to lean Republican and they are also poised to be key beneficiaries of Trump’s “America first” policies. While the election had not yet been conducted when the survey was snapped, polls were showing his chances were improving. Around 70% of the rise in the NFIB’s optimism index was due to four components: good time to expand, expectations for the economy, sales, and earnings.

Owners also note the upcoming holiday season as a source of optimism.

There is, however, one aspect of the survey that takes the gilt off of the gingerbread: credit conditions faced by small businesses are restrictive, despite a slight improvement. With markets anticipating that Trump policies could be inflationary, “higher for longer” is back in the airwaves. This could prolong the pain for small businesses that were quite eagerly awaiting a loosening in financial conditions.

Source: Bloomberg, BIL

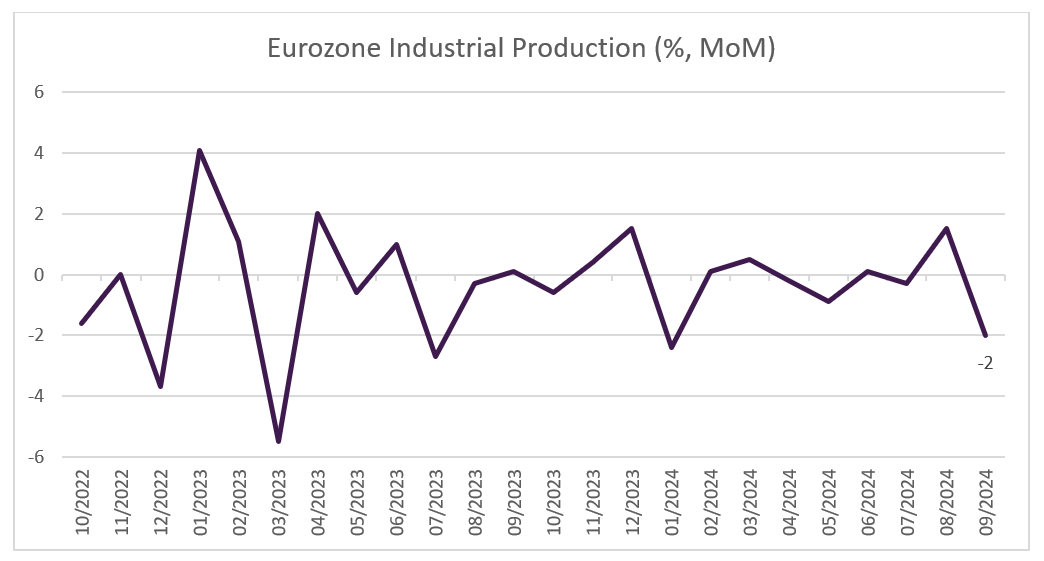

Eurozone Industrial Production down by 2%

Industrial production in the Eurozone fell by 2% in September, compared to August. Production fell for energy and capital goods, was unchanged for intermediate goods, slowed for durable consumer goods and rose for non-durable consumer goods. Germany reported a significant fall in production of 2.7%. France and Italy also recorded falls, while Spain recorded a rise of 0.9 %. Compared with a year earlier, industrial production in the Eurozone fell by 2.8%.

Source: Bloomberg, BIL

In November, the ZEW indicator of economic sentiment in the Eurozone fell by 7.6 points to 12.5, well-below expectations. This is yet another in a series of disappointing data releases that do little to inspire confidence in the outlook for the bloc’s economy.

China’s Singles’ day nudges Chinese consumers to start spending

Every year on 11 November, China celebrates Singles' Day. This unofficial Chinese holiday, dedicated to people who are not in a relationship, started as a way for single people to treat themselves to gifts and organise social gatherings, but has grown into one of the world's biggest shopping days. The event is no longer limited to 11 November and can now extend over several weeks. Sales growth during the holiday is seen as a strong indicator of consumer confidence, something that has been in short supply in China recently.

China has struggled with weak consumer demand in a challenging economic environment. The direction of the Chinese economy has been seen as too uncertain to convince consumers that they can comfortably spend their money. Major stimulus announcements from Beijing have boosted equity markets but have failed to inspire consumer confidence. The election of Donald Trump has brought these doubts into sharper focus, with fears that Trump's trade tariffs will further damage an already struggling economy.

However, the Singles' Day sales offered by some of China's biggest e-commerce companies appear to have sparked some spending, with record numbers of shoppers. Data provider Syntun estimates that sales on major e-commerce platforms increased by more than 26% during this year's event. While this boost in spending is likely to be temporary, is shows some motivation of Chinese consumers, perhaps strengthening the case for Beijing to announce further fiscal stimulus.

Economic calendar for the week ahead

Monday – Eurozone Balance of Trade (September). Switzerland Industrial Production (Q3).

Tuesday – Switzerland Balance of Trade (October). Eurozone Inflation Rate (Final, October). US Housing Starts (October).

Wednesday – Japan Balance of Trade (October). UK Inflation Rate (October).

Thursday – EU New Car Registrations (October). US Jobless Claims, Existing Home Sales (October). Eurozone Consumer Confidence (Flash, November).

Friday – Japan Inflation Rate (October). UK GfK Consumer Confidence (November), Retail Sales (October). Eurozone, Germany, UK, US Composite, Manufacturing, Services PMI (Flash, November). US Michigan Consumer Sentiment (Final, November).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

April 7, 2025

Weekly InsightsWeekly Investment Insights

So-called “Liberation Day” has catalysed a global market selloff, with US President Trump announcing sweeping new US tariffs, including a baseline 10% tariff on...

April 7, 2025

NewsMarket Update – 7 April 2025

The market sell-off following the announcement of new trade tariffs continues as investors try to assess Trump’s next move and the impact on the global...

April 3, 2025

NewsUS Tariff Policy Signals New Era of P...

US announces higher-than-expected trade tariffs Market reaction was clearly risk-off but still manageable Uncertainty is here to stay. As with previous announcements, Trump could still...

April 2, 2025

BILBoardBILBoard April 2025 – Tariffs, turbul...

Written as at April 1 The first quarter of 2025 was anything but smooth. Market volatility surged, equity markets diverged, bonds offered little in the...

March 28, 2025

Weekly InsightsWeekly Investment Insights

Another week, another set of changes to US trade policy – and that’s before the April 2 deadline where reciprocal tariffs on several trading partners...