Research

Choose Language

March 24, 2025

Weekly InsightsWeekly Investment Insights

Last week was dominated by central bank meetings, with the Fed, the Bank of England, Sweden's Riksbank and the Bank of Japan holding rates steady amid heightened global uncertainty. Only the Swiss National Bank cut rates by 25bp. This was all in line with market expectations, making market movements following the announcements rather limited. In the US, however, equity markets rallied toward the end of the week as investors found Powell’s statement largely positive. Gold continued to shine, rising to a record high after the Fed's announcement.

Central banks and companies around the world are waiting to see how tariffs will play out and what impact they will have on inflation and growth. Trump is set to unleash a new wave of "reciprocal" tariffs on 2 April. While no tariffs would be the widely preferred situation, even a clear announcement on what tariffs will be imposed could provide some stability and allow companies to adjust their strategies accordingly.

Weekly Highlights

The Fed holds rates steady in March

On Wednesday last week, the Federal Reserve kept interest rates steady at 4.25-4.5% and signalled two possible cuts in 2025. It also updated its economic forecasts, estimating that economic growth in 2025 will be 1.7% (down from 2.1%), while foreseeing higher inflation - headline PCE for 2025 is seen at 2.7% (up from 2.5%). It also announced that starting next month, it will slow the pace of its balance sheet drawdown amid an ongoing impasse over lifting the government’s borrowing limit.

As mentioned in the introduction, the Fed is in a 'wait and see' mode, waiting for more clarity on the economic impact of tariffs before altering its policy pathway. Despite noting the increased uncertainty, the Fed said it sees another 50 basis points of rate cuts this year. However, Federal Reserve Chairman Jerome Powell stated that “If the economy remains strong, and inflation does not continue to move sustainably toward 2%, we can maintain policy restraint for longer “. Powell called the inflationary impact of tariffs “transitory”—a phrase that markets greeted with skepticism, recalling the Fed’s earlier misjudgment of post-pandemic price pressures.

Equities rose after the announcement as investors saw the move as less hawkish than expected. It also triggered a relief rally in US Treasuries.

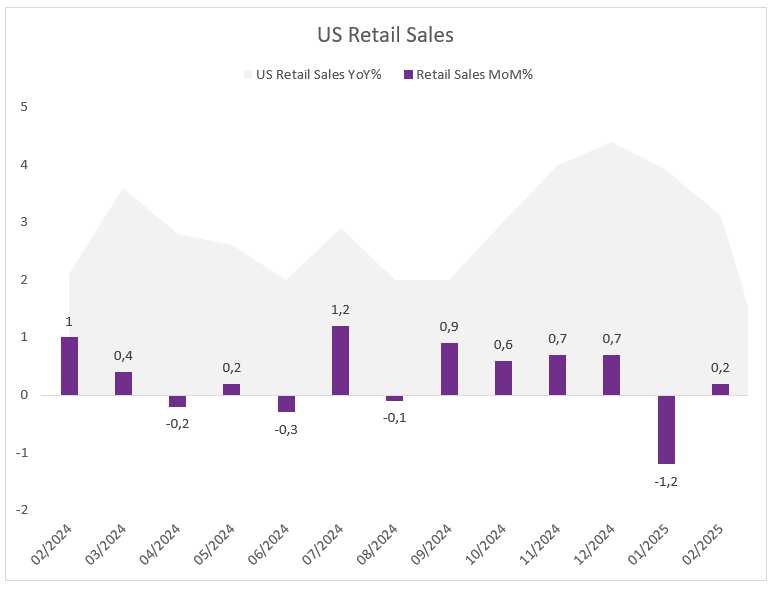

US retail sales recover from a two-year low

Consumer spending has been the main driver of growth in the US over the past year, but recent consumer confidence readings cast doubt on whether this momentum will continue throughout 2025.

Rewinding back to January, retail sales slumped by the most in two years at a downwardly revised -1.2% MoM pace, with sales falling across 9 of 13 categories. Shopping activity was likely affected by the wildfires in Los Angeles, as well as severe snowstorms elsewhere in the country.

However, retail sales attempted a partial recovery in February, rising by 0.2%. The reading was still below expectations of a 0.6% rise, however. Declines in sales at eating and drinking places, petrol stations, clothing stores, motor vehicle and parts dealers, among others, were offset by increases in sales at online stores, health and personal care stores, food and beverage stores, general merchandise stores and building material stores.

The report comes amid heightened concerns about the outlook for economic growth, with tariff announcements weighing on sentiment at a time when stubborn inflation and high borrowing costs are still weighing on consumers.

Households and businesses alike are expected to be more cautious about spending as they await greater clarity on the economic outlook.

Source: Bloomberg, BIL

Thursday on Threadneedle Street

Across the Atlantic, the Bank of England held rates steady on Thursday, while emphasising a gradual and careful approach. The Monetary Policy Committee voted 8 to 1 to keep the benchmark policy rate at 4.5% and markets perceived the meeting as somewhat hawkish. The BoE faces still-strong wage growth, and the fact that firms are more aggressive in passing on increasing costs while the domestic economy is weak. Potential tariffs add to an already-complicated stew. "There's a lot of economic uncertainty at the moment," Governor Andrew Bailey said in a statement. He said the BoE still believed rates would fall gradually but it would look "very closely at how the global and domestic economies are evolving at each of our six-weekly rate-setting meetings."

With inflation stuck well above the 2% target, hitting 3% in January, the central bank also updated its inflation forecast for the year, estimating that inflation will reach 3.75% at its peak. This is in part due to the tax hikes for employers that is set to come in force in April.

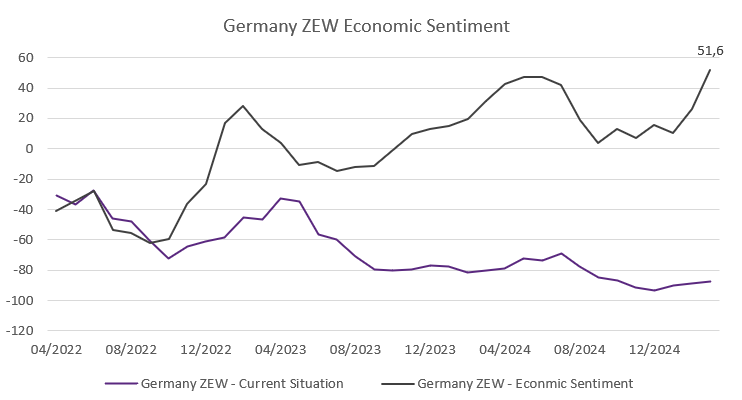

Economic sentiment in Germany on the rise

The ZEW Indicator of Economic Sentiment for Germany jumped 25.6 points to 51.6 in March, the highest level since February 2022. Driving optimism is Germany’s commitment to a significant fiscal expansion, including a EUR 500 billion infrastructure fund over 12 years and the easing of its constitutionally mandated debt break to enable higher borrowing.

In particular, the outlook for metal, machinery, and steel production is showing signs of improvement. The ECB’s latest interest rate cut, has also helped boost sentiment about financial conditions for both households and businesses.

Source: Bloomberg, BIL

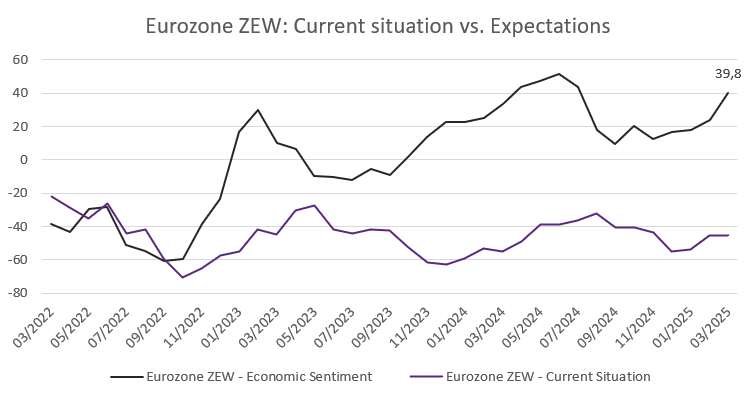

On the Eurozone level, economic sentiment rose to the highest in 8 months to 39.8 in March.

Source: Bloomberg, BIL

Swiss National Bank cuts rates to 0.25%

The Swiss National Bank (SNB) swam against the tide last week and cut interest rates by 25 basis points, bringing the key interest rate to 0.25%. This is the lowest rate since September 2022 and comes amid low inflation, a strong Swiss franc and economic uncertainty from Trump's trade tariffs. Inflation has fallen from 0.7% in November to 0.3% in February, largely due to lower electricity prices. The rate cut is aimed at preventing a further decline in Swiss inflation and a further strengthening of the Swiss franc.

The SNB expects the economy to grow by 1-1.5% in 2025, driven by higher wages and low interest rates, while noting that weaker global demand could weigh on trade.

The Swiss franc weakened slightly against both the euro and the dollar following the announcement.

Calendar for the week ahead

Monday – US, Japan, Eurozone, UK Flash Manufacturing PMI.

Tuesday – Eurozone Car Registrations. Germany IFO Business Climate. US House Price Index, Richmond Fed Manufacturing Index

Wednesday – UK Inflation and Spring Economic Sentiment. France Unemployment data. US Durable Goods Orders.

Thursday – China Industrial Profits. Eurozone M3 Money Supply. US GDP Growth (Q4, Final Print), Weekly Jobless Claims, Pending Home Sales. Spain Business Confidence.

Friday – Germany GFK Consumer Confidence. UK Retail Sales, GDP Growth (Final, Q4). France, Spain Inflation (Preliminary, March). France Household Consumption. Germany Unemployment. Italy Business and Consumer Confidence, Industrial Sales. Eurozone Economic Sentiment. US Personal Income and Spending and PCE Price Index, Michigan Consumer Sentiment (Final, March).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

March 27, 2025

NewsPotential economic impacts of peace i...

As negotiations continue with a view to reaching a possible peace agreement in Ukraine, hopes are growing for an economic recovery in Europe. Markets...

March 26, 2025

NewsAn economic Equinox in the US

On Thursday March 20th, the Northern Hemisphere marked the Spring Equinox. During this phenomenon, we experience an identical amount of daylight and night-time hours due...

March 17, 2025

Weekly InsightsWeekly Investment Insights

It’s St. Patrick’s Day, but the colour green has been rare on our Bloomberg screens over the past week, with trade frictions, growth fears and...