Research

February 24, 2025

BILBoardBILBoard February 2025 – Repainting the global trade system

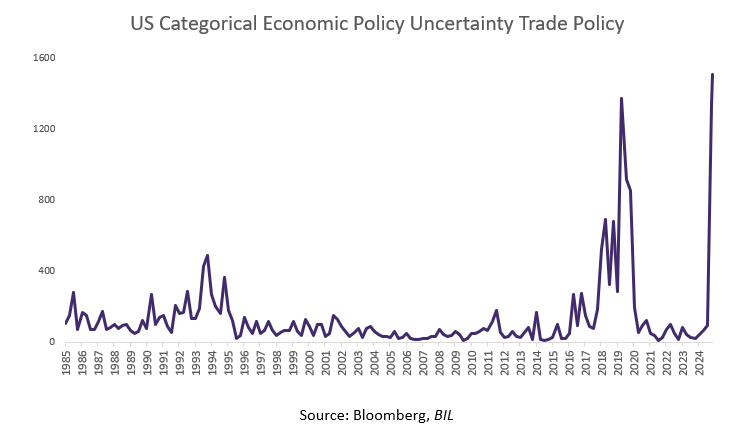

When President Trump took office on January 20th, it was clear that tackling the US trade deficit would be a high priority. This is not only due to his frequent discourse on the subject, but also because the Republicans currently hold the slimmest majority in the House than any administration has had in a century, necessitating the support of at least seven Democrats to advance most legislation in the Senate. This situation compels the President to rely on executive orders as a means to bypass Congressional hurdles. As a result, he is now concentrating on issues such as geopolitics, immigration, and trade, in contrast to 2016, when he kicked-off his term with a focus on the domestic economy—for that, you largely need Congress on side.

So, while markets had a clue about what Trump might do in his first 100 days, more important was the how. A genuine concern was a set of broad-brushed and indiscriminate tariffs on America’s allies and adversaries alike; tariffs implemented with the same reckless abandon as Jackson Pollock splashing paint across his canvas, creating chaotic effects. However, it seems that Trump is, in fact, “painting-by-numbers”, having signed an action for his staff to design a plan to impose tariffs on US trade partners based on “reciprocity”. The vernissage for the unveiling of the new US trade architecture is scheduled for early April.

In the meantime, markets have embraced the approach as it appears to be more measured and also affords time for negotiation. As of today, it is generally emerging market countries with limited trading relationships that impose meaty tariffs on US goods. Canada and Mexico have 0% tariff rates with the US, the EU has just a mere +1.2 percentage point (pp) tariff rate differential with the US, while for China it is even negative.[1] Given that Canada, Mexico, China and the EU make up more than 60% of US imports, the overall impact therefore might be manageable. However, it could be more dramatic if the administration proceeds with the inclusion of VAT and other non-tariff barriers in its calculations. For now, it seems the market senses that the extreme starting point and extended timeline might in fact just be a canvas from which Trump can initiate negotiations.

Indeed, of the tariffs that Trump has announced, he has only implemented one of them as of today: 10% tariffs on China, while subsequently commenting that a trade deal is “possible”. Tariffs on aluminum, steel, Canada, Mexico and Colombia were all pushed out, leaving time for concessions to be struck.

Trump 2.0 will no doubt drive a realignment in global supply chains. However, knee-jerk investing based on trade announcements is a risk as the picture currently looking like a Chagall, full of tricks and pranks. We, like the Fed, await more clarity before acting further in our portfolios. The key problem is that if uncertainty persists for too long, that alone could start to hinder corporate confidence, investment and economic activity.

The Macro Landscape

After the US recorded growth of 2.8% in 2024, consensus expectations are for a still-respectable pace of 2.2% in 2025. Consumption is the key driver of US exceptionalism but evidence suggests that households are beginning to tighten their belts, with a resurgence of inflation fears weighing on confidence. For now, we think that as long as the labour market remains resilient, it will put a floor under spending. The hope is that business-friendly policies will catalyse an upturn in the corporate sector, keeping activity – and employment dynamics – supported. Sentiment is improving, primarily in the manufacturing sector, where new orders are on the rise, and where business confidence hit a 34-month high in January.

The flipside is that proposed policies might fan inflation, potentially derailing the Fed’s easing campaign. Already, headline inflation is on the rise, having increased every month since September, hitting 3.0% YoY in January. The Fed has already revised the number of rate cuts that it projects for this year from four to two. Futures markets price in one rate cut for this year, and a second cut is priced as a coin toss. Minutes from the Fed’s January meeting revealed a certain nervousness about the economic consequences of President Trump’s policies. With the Fed likely on hold for the months to come, corporate earnings will likely come to the fore.

Things look promising on that front: of the S&P 500 companies that had reported their results at the time of writing, EPS growth was 16.9% on aggregate. If this rate holds, it will be the highest reported growth since Q4 2021. The fruitful earnings season has compelled analysts to make upwards revisions to future expected earnings.

In Europe, while the macroeconomic situation remains challenging, certain aspects are allowing markets to breath a collective sigh of relief: PMIs give hope that the manufacturing sector is bottoming out, Germany might soon have a government capable of action, a ceasefire in Ukraine could be on the cards, and France has managed to pass a 2025 budget. That said, the Euro Area continues to lag the US, and economists expect growth of just 0.9% this year. A weak economy, and signs of cooling in the job market should keep the ECB on track for sequential rate cuts in the coming months.

Looking to China, little has changed since our assessment in last month’s BILBoard, even if market sentiment was positively impacted from debut of “DeepSeek”. In all, 2025 will be another year in which Beijing will try to boost growth and domestic consumption. We await the annual “two sessions” parliamentary meeting on March 5 for a clearer roadmap.

Investment Strategy

While being neutral on equities overall, within that exposure, we maintain a preference for the US and a bias towards small caps as they could benefit from America First policies.

Worth noting, is that for Q1 2025, S&P 500 companies with more international revenue exposure are projected to report lower earnings than equivalents with more domestic revenue exposure. The estimated earnings growth rate for the S&P 500 overall for Q1 2025 is 8.1%. For companies that generate more than 50% of sales inside the US, it is 9.1%. For companies that generate more than 50% of sales outside the US, that figure falls to 6.6%.

With the market now considering the glass half-full when it comes to Europe, we have benefitted from having a relatively large proportion of European equities versus what we observe among other institutional investors. In light of better-than-feared corporate earnings and hopes for an improving macro picture, we are monitoring developments in order to weigh whether we would like to add further.

In the Fixed Income space, investment grade forms the cornerstone of our exposure, complimented by high-yield to boost income. With yields at depressed levels, out-of-the-box thinking is increasingly essential in order to introduce new income sources into portfolios.

This month, in Defensive and Low profiles, we reduced Sovereign exposure (by 3% and 2%, respectively), allocating the proceeds were equally to corporate hybrids and CoCos (high-yield). These products offer reduced sensitivity to interest rate fluctuations due to their lower duration profiles, and a more attractive risk-return trade off.

In Defensive profiles, we implemented a decision made in January to switch 4% of the investment grade exposure into structured credit. The asset class offers a more attractive yield pick-up, while increasing portfolio diversification given that structured credit has low correlation to other fixed income asset classes. The floating rate nature of structured credit means that duration risk in the portfolio is reduced.

The art of the deal

For the months to come, investors will have the increasingly difficult challenge of focusing on fundamentals amid a flurry of headlines and a flow of unconventional communication from the new US administration. At BIL, we strive to help our clients separate noise from signal, with the aim of achieving stable portfolio returns over time. While Trump’s messages are oil-painting bold, the past has shown, that the outcome can sometimes be watered down, becoming more like an aquarelle. He himself writes in “The Art of the Deal”: I never get too attached to one deal or one approach. For starters, I keep a lot of balls in the air, because most deals fall out, no matter how promising they seem at first.

[1] https://www.fitchratings.com/research/sovereigns/us-reciprocal-trade-policy-widens-range-of-potential-tariff-outcomes-18-02-2025

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

April 23, 2025

NewsThe Gold Rush

In recent months, gold has experienced remarkable momentum, solidifying its position as a preferred safe haven asset. Contrary to what the collective imagination suggests,...

April 7, 2025

Weekly InsightsWeekly Investment Insights

So-called “Liberation Day” has catalysed a global market selloff, with US President Trump announcing sweeping new US tariffs, including a baseline 10% tariff on...

April 7, 2025

NewsMarket Update – 7 April 2025

The market sell-off following the announcement of new trade tariffs continues as investors try to assess Trump’s next move and the impact on the global...

April 3, 2025

NewsUS Tariff Policy Signals New Era of P...

US announces higher-than-expected trade tariffs Market reaction was clearly risk-off but still manageable Uncertainty is here to stay. As with previous announcements, Trump could still...