Research

Choose Language

November 2, 2020

BILBoardBILBoard October 2020 – Weathering the pandemic

Overall, as the world emerges more quickly

than anticipated from one of the worst recessions on record, growth forecasts

have improved; the IMF now expects the global economy to experience a 4.4%

contraction in 2020, 0.8% better than predicted in June. This is largely thanks

to floods of fiscal and monetary stimulus and the containment of the virus in

China and other Asian countries. However, a Corona-shaped cloud still hangs

over the economy, threatening to rain on the recovery, undermining confidence,

consumption and investment. Some countries are better equipped to weather the

virus than others (from both a medical and policy standpoint) and, as such, a

very uneven recovery is playing out.

In the US, despite three million active

cases of the virus, stabilization is at play thanks to the Treasury and the

Federal Reserve. Business confidence is improving and factory activity rose for

four consecutive months before September’s moderation of -0.6% (which shows it

may be difficult to keep pace while the virus persists). On the consumer side,

sentiment increased in October, retail sales are stronger than they were before

the pandemic (concentrated online, in supermarkets and at building material

stores) and the real estate market is particularly buoyant. However, continued

confidence somewhat hinges on new fiscal stimulus to further support the

economy and the labour market. While the unemployment rate has fallen to 7.9%, long-term

unemployed (unemployed for 27 weeks or more) figures are creeping up, most recently

by 781,000 to 2.4 million, and labour market slack has weakened employee bargaining

power when it comes to wages. Inflation is still on the rise, reflecting an

improving economic situation, however we haven’t seen a risk of a sudden spike

that would instigate a policy pivot from the Fed (especially under its new

average inflation targeting). The elections are generating some anxiety and may

give rise to short-term volatility (especially if the outcome is disputed), but

ultimately, economic cycles are much more important for asset classes than the

composition of the US Government. In terms of the currency, we believe the

picture less supportive for the US dollar due to the cumbersome twin deficits

which could expand further if we see a Democratic sweep in the elections.

In the eurozone, the IMF expects a

contraction of -10.2%. Indeed, more rain could be on the forecast, as we wait

for datapoints showing how consumer behavior has been affected by the second

round of lockdowns and restrictions. Already, a loss of momentum in the industrial sector is clear,

and the pandemic has left a puddle on the labour market, with the unemployment rate on the rise since March (most recently 8.1%)

while inflation has all but evaporated (-0.3% in September), in part due to the

stronger euro.

In China,

with the virus almost snuffed out, the clouds have receded, making way for

economic sunlight. The country is an outlier in that it is expected to post positive

growth in 2020; the IMF predicts 1.9%, followed by 8.2% in 2021. Demand (external

and domestic) is coming back and China is now reshoring certain activities that

had been outsourced.

Other emerging markets are still in the thick fog of the pandemic. The IMF predicts growth of -8.1% in Latin America, as “the legacies of the pandemic cloud an already uncertain outlook”, while in India, for example, the economy is projected to contract by -10.3%. Oil exporting countries are at a particular disadvantage.

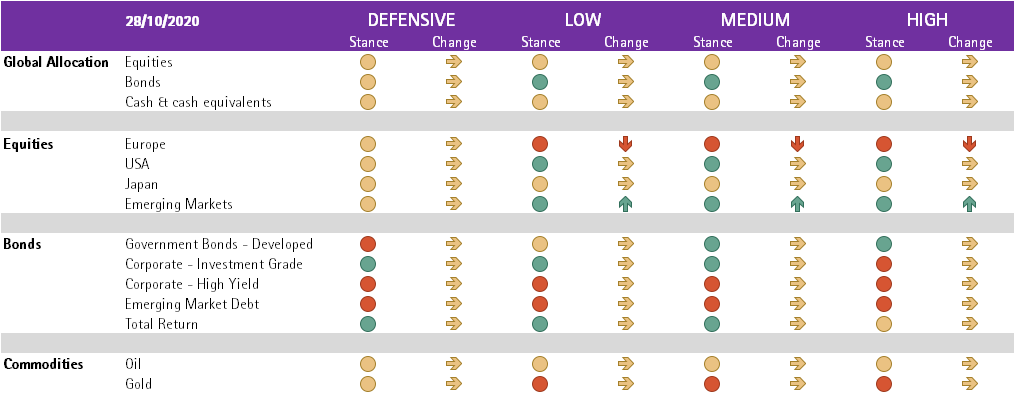

Fixed Income

We are maintaining our previous

allocations within the bond space, with a preference for high quality corporate

bonds in both developed markets and within our Emerging Market allocation.

While we’ve maintained a layer of governments

as a windbreaker in times of heightened volatility, we are generally reluctant

on this asset class, especially in the US and on longer duration. Polls suggest

that the Democrats could take victory in the US election. If they do, we could see

a much larger stimulus package (c. $2 trillion) than may have been expected

under Republican charge, which could in turn drive rates higher. As such “short

Treasuries” is now a consensus trade.

We like corporate bonds given the continued support of central banks. The ECB is expected to continue buying bonds at a pace of up to EUR 10 billion per month. Economists expect more stimulus to be announced in December 2020 and an extension of the emergency program to end-2021. In the US, the bond market is now standing on its own two feet and the Fed has been able to dial down its bond buying, using only a fraction of its firepower. Despite the fact that the Fed’s buying is mostly symbolic, if it doesn’t extend the program which is set to expire in December, there is a risk of volatility.

High-yield bonds have been trading sideways. In

Europe, default rates are low, while being slightly higher in the US (however 4/5

of defaults occurred in the beleaguered energy sector). We are selective on

this asset class, preferring companies that have not saddled themselves with

too much debt. In the emerging market debt space, corporates are still the most

attractive tranche.

Equities

Maintaining an overweight in the US and switching part of our European

exposure to China.

Despite

rising infection levels, US equity markets were stable up to the last week of

October and following September’s correction. The Q3 earnings season has been

better than feared (over 80% of companies on the S&P 500 have reported a

positive surprise), however is still on track to post the second worst set of

results since the 2008 financial crisis, and guidance remains opaque. The US has

strong prospects given that it is the region where the most prominent growth

and “stay at home” beneficiaries are located. It is admittedly expensive, with

hopes around new stimulus inflating valuations even further – so the challenge will be for companies to deliver on the earnings

front in 2021. The US is the only region to have a minor positive

revision amongst analysts, however this has started to level off as they grow a

little more sceptical – something we are paying close attention to, especially

as earnings results roll out.

With the eurozone underperforming on almost every

front, we have gone even more underweight, switching a proportion of our

holdings to Chinese equities. Accelerating

reforms in China are broadening access to foreign investors, lifting growth

prospects while sectors like technology, healthcare and consumption are driving

returns.

In

terms of style, “lower for longer” interest rate policies are supportive of

growth and quality stocks. In terms of sectors, we like healthcare, consumer

staples and IT, as well as some late cyclicals such as materials and utilities

which have enjoyed strong revisions. Due to wide-ranging dispersions in

performance, selectivity is key, and we still prefer to identify top performers

within sectors, rather than betting on sectors as a whole.

Commodities

Despite the short-term consolidation in

September, we are constructive on gold over the longer term. Bullion ETFs have

received record inflows and the price is on an uptrend – above its 100-day

moving average. Higher inflation expectations remain supportive.

We are negative on oil. Even though demand

has picked up recently, driven by China, it will likely come under pressure

again as governments unveil new restrictions on activity. The second round of lockdowns

has also limited OPEC’s flexibility to loosen supply, as it planned to do in

January 2021.

Conclusion

In Japan there are fifty different words to describe rain. There are just as many different rates of recovery playing out around the world, and we aim to position ourselves in locations that are faring best – namely the US and China. In the coming quarters, the trajectory of the economy will depend largely on countries’ ability to contain the virus, but come rain or shine, a well-diversified portfolio comprising high quality assets is the best way to weather the storm until blue skies return.

Change: Indicates the change in our exposure since the previous month’s asset allocation committee

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

January 10, 2025

NewsVideo summary of our Outlook 2025

2024 - The US economy exhibited impressive strength powered by consumption, while Europe struggled with weak demand and a protracted manufacturing downturn 2025 - The...

December 27, 2024

NewsBIL Investment Outlook 2025 – T...

Introduction from our Group Chief Investment Officer, Lionel De Broux As the oldest private bank in Luxembourg, we’ve been managing clients’...

December 20, 2024

Weekly InsightsWeekly Investment Insights

Having spent ten straight days decked out in red, the Dow Jones Industrial Average index recorded is longest losing streak since 1974. Other global...

December 13, 2024

Weekly InsightsWeekly Investment Insights

It has been a big week for France, with Notre Dame finally reopening after five years of reconstruction, and Francois Bayrou being named France’s...

December 9, 2024

Weekly InsightsWeekly Investment Insights

December is here, and while the cold, dark days may not be everyone's cup of cocoa, the festive spirit is starting to set in....