Research

April 2, 2025

BILBoardBILBoard April 2025 – Tariffs, turbulence and tactical shifts

Written as at April 1

The first quarter of 2025 was anything but smooth. Market volatility surged, equity markets diverged, bonds offered little in the way of refuge, and investors were reminded just how quickly sentiment can shift when policy uncertainty meets geopolitical strain. This edition of the BILBoard focuses on how we’re interpreting the current landscape and positioning portfolios for what lies ahead.

Market Recap: A Volatile Quarter Defined by Trade Tensions

Thus far, 2025 has been characterised by elevated volatility and notable equity declines—particularly in the US. At the heart of the turbulence lies a familiar theme: trade uncertainty.

Tariffs, often introduced or reversed with little warning, have amplified unpredictability for global businesses and investors. The rapidly evolving policy landscape presents operational challenges for companies and renewed pricing concerns for US consumers—many of whom no longer have a pandemic-era savings buffer.

Amid rising stagflation fears in the world’s largest economy, US equities saw their sharpest quarterly drop in nearly three years. The S&P 500 fell 4.6%, while the Nasdaq slid more than 10%.

In contrast, European equities gained around 5%, boosted by optimism around a potential resolution in Ukraine and the announcement of large-scale fiscal spending—particularly favouring aerospace and defence stocks.

What boosted equities was extremely painful for bond investors. Defence spending plans across the EU (with a EUR 800Bn package now in the pipeline), and the fiscal policy pivot in Germany, exerted strong upwards pressure on yields. German government bonds experienced their worst sell-off in decades.

In a quarter that contained more questions than answers, one asset stood out: gold. As a traditional safe haven, it surged to as USD 3,128 a troy ounce, a fresh record.

Macro View: Slowing Growth, Shifting Policy

Eurozone growth forecasts remain subdued, with defence spending unlikely to deliver an immediate impact given the time it will take to scale up domestic defence production. At its latest monetary policy meeting, the ECB lowered its growth forecast for this year from 1.1 to 0.9%, citing increased uncertainty. At the same time, it hinted it may be near the end of its easing cycle, as inflation cools and governments prepare to open the spending taps.

In the US, while soft data has been volatile, hard data remains relatively resilient for the time being, with the labour market still exhibiting residual strength. The impact of tariffs remains uncertain, but pro-growth policies are still expected. Officials have commented that the revenue from tariffs will be used to “give the largest tax cut in American history” and other supportive measures are forthcoming, such as the recent Executive Order aimed at increasing American production of critical minerals like uranium, copper, potash and gold. The Fed foresees slower growth this year (1.7%) and higher inflation (PCE at 2.7%), while its dot-plot continues to show two more rate cuts before the end of 2025. Aggressive trade tariffs could alter that pathway if price pressures continue to heat up.

In China, measures announced to boost consumption are thus far perceived as insufficient to cushion the economy against the potential impact from rising trade tensions.

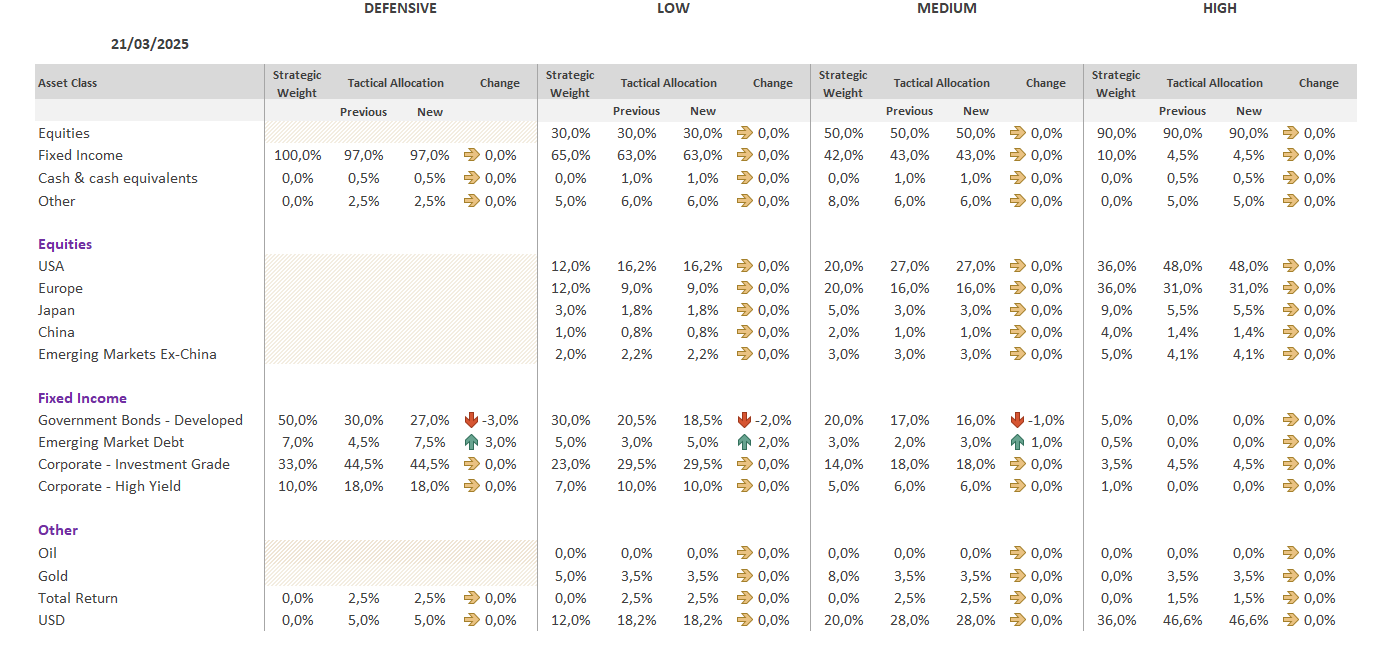

Investment Strategy

At the heart of our investment strategy lies a consistent philosophy—stability in our convictions, while being flexible enough to adapt to evolving markets.

Equities

Firstly, we maintained our overweight on US equities, and actually rebalanced our exposure upwards in order to maintain our target weights after the market correction. After several years of unusually low volatility, a return to historical norms can be unsettling—but also creates opportunity. Insofar as now, fundamentals remain sturdy enough to comfort us in our stance. Moreover, the earnings hurdle for US companies is now lower, and we also note that company insiders are buying the stocks of their firms at the fastest pace unseen since June. We also note our hedging strategy, initiated at the end of last year proved beneficial, as it expired on 20 March in the money, at one of the S&P 500’s low points of the year so far.

When it comes to European equities, after strong performance, we locked in gains and reduced positions back to our neutral target—believing much of the good news is already priced in. Tariffs are clearly a major overhang.

Within our Sector preferences, we have made the following updates to reflect the shifting environment:

- US Consumer Staples: Upgraded to Neutral

Supported by a weaker USD and solid earnings. Valuations are attractive, though trade risks remain a concern. - European Consumer Discretionary: Upgraded to Neutral

Signs of recovery in luxury and autos, with improving sentiment and economic data. Some tariff risk is already priced in. - European Communication Services: Upgraded to Positive

Strong regulatory tailwinds and less exposure to tariffs make this a compelling defensive play, with 5G and digital infrastructure as growth drivers. - European Financials: Upgraded to Positive

Yield curve steepening and ongoing buybacks are strong tailwinds. Despite lower dividend yields, the sector remains robust. - European Industrials: Upgraded to Positive

Buoyed by improving PMIs and government investment in defense and infrastructure—especially in Germany. - European Healthcare: Downgraded to Neutral

Taking profits after strong performance. Headwinds include currency shifts, US policy uncertainty, and patent expirations. - European Real Estate: Downgraded to Neutral

Rising bond yields and a market shift toward infrastructure make the near-term outlook challenging. - European Utilities: Downgraded to Neutral

Electrification trends remain supportive, but higher yields present a headwind for this rate-sensitive sector.

Fixed Income

European Investment Grade bonds continue to serve as the cornerstone of our fixed income allocation. This proved beneficial during recent market turbulence – while US credit spreads widened in tandem with the equity market sell-off, European spreads were relatively stable. European credit still exhibits strong technicals and fundamentals. Looking ahead, the segment should be supported by new fiscal spending plans. Within Investment Grade, we see financials and corporate hybrids as the most attractive niches.

We compliment this exposure with a helping of high-yield to boost income in portfolios, whilst being diligent when it comes to credit risk. In that sense, we prefer the more defensive nature of European high-yield. In the US, loans look better poised than plain-vanilla high-yield.

Believing that pressure on European rates could remain due to the new fiscal stance in the Eurozone, we reduced Sovereign exposure in Defensive, Low and Medium profiles. The proceeds were allocated to Emerging Market Debt (EMD). We like hard currency bonds which have performed better, benefiting from substantial spread tightening and attractive carry, particularly among weaker countries. By increasing our exposure to EMD, we also increase exposure to the US curve. With the Fed slowing the pace of its balance sheet drawdown, some pressure on Treasury yields should ease.

Final Thoughts

While it was well known that tariffs were among President Trump’s favoured policy tools, the manner in which trade measures are now being introduced—often abruptly and without consultation—has taken both allies and adversaries by surprise. Investors, too, have been caught off guard, not only by the policy shifts themselves, but by the administration’s apparent willingness to tolerate market volatility and even risks to US economic growth.

The Q1 sell-off reflects a rising risk premium as markets adjust to this new, less predictable environment. Yet, amid the uncertainty, our philosophy remains clear: we remain focused on fundamentals and lean into our convictions, while staying agile and adaptive.

From rebalancing regional equity exposures and increasing our allocation to Emerging Market Debt, to refining our sector positions in response to macro and policy shifts, we continue to navigate 2025 with both vigilance and confidence—remaining alert to risk, but equally attuned to opportunity

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

April 23, 2025

NewsThe Gold Rush

In recent months, gold has experienced remarkable momentum, solidifying its position as a preferred safe haven asset. Contrary to what the collective imagination suggests,...

April 7, 2025

Weekly InsightsWeekly Investment Insights

So-called “Liberation Day” has catalysed a global market selloff, with US President Trump announcing sweeping new US tariffs, including a baseline 10% tariff on...

April 7, 2025

NewsMarket Update – 7 April 2025

The market sell-off following the announcement of new trade tariffs continues as investors try to assess Trump’s next move and the impact on the global...