BIL INVESTMENT INSIGHTS

Geopolitical tensions returned to the forefront of financial markets last week. After tankers were reportedly targeted in the Strait of Hormuz, the US launched a new round of strikes against Iran on Tuesday, and revoked a licence that had allowed the country to export oil, raising concerns about the durability of the fragile ceasefire.

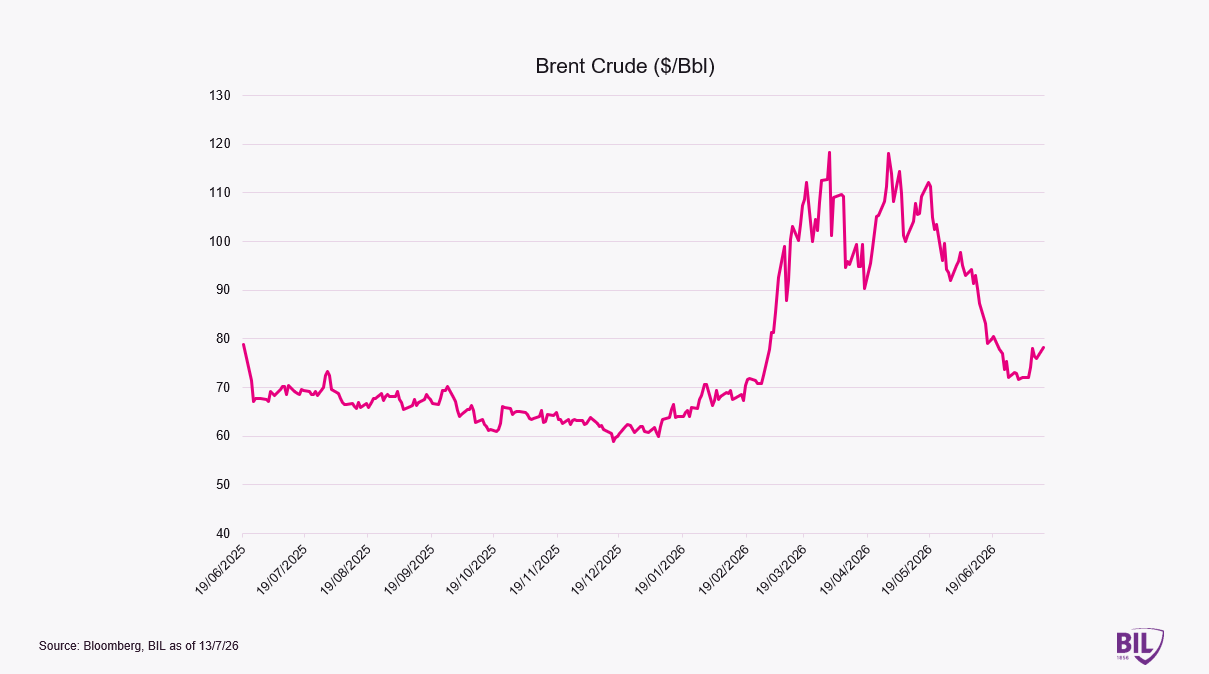

Fighting continued over the weekend, leaving uncertainty over the operational status of the Strait of Hormuz, a critical artery for global energy supplies. As a result, Brent crude rose to around USD 79 per barrel on Monday morning, although remaining well below the peak of USD 118 reached during the height of the crisis in late April.

Diplomatic efforts have continued in parallel, but negotiations remain complicated by competing priorities. On one hand, the Trump administration is seeking a swift reopening of shipping routes through the Strait to alleviate energy market pressures ahead of the US midterm elections. On the other, Iran remains reluctant to relinquish leverage over one of the world's most strategic waterways.

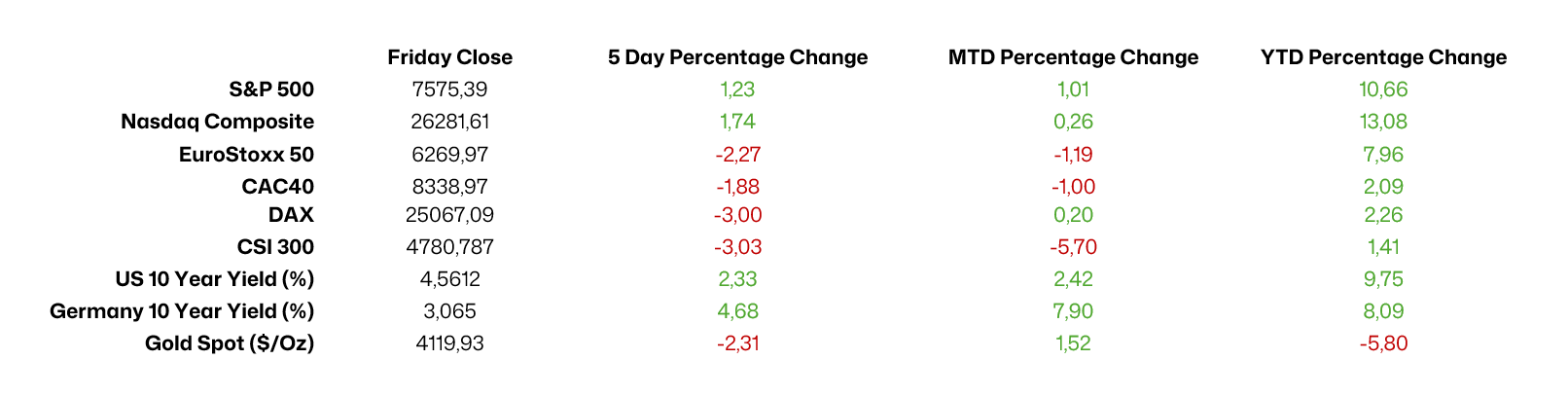

Equities experienced some volatility throughout the week, though US markets proved resilient, with both the S&P 500 and Nasdaq ending higher, supported by renewed strength in semiconductor and AI-related stocks. European equities, by contrast, closed lower as investors reassessed the inflationary and monetary policy implications of renewed tensions in the Middle East.

The minutes from the Federal Reserve’s June 16-17 meeting revealed that officials are skewing more hawkish, and highlighted an uncertain balance of risks.

Against the current backdrop, markets are increasingly pricing in the possibility of further rate hikes on both sides of the Atlantic, potentially as early as September. In France, the 10-year government bond yield briefly touched its highest intraday level since 2009. Inflation concerns were likely amplified by domestic political developments, including news that Marine Le Pen would be eligible to stand in the next presidential election.

Looking ahead, attention is now turning to the second-quarter earnings season, where expectations remain elevated. In the US, consensus forecasts point to EPS growth of around 22%, while European companies are expected to deliver earnings growth of approximately 12%, which would mark the strongest performance in three years. Investors will also closely monitor upcoming US inflation data and testimony from Kevin Warsh, both of which could provide further insight into the outlook for monetary policy and interest rates.

Source: Bloomberg, BIL as of 13 July

Macro Snapshot

IMF cuts global forecast for this year, envisions recovery thereafter

The International Monetary Fund (IMF) has slightly downgraded its global growth forecast for 2026, lowering it from 3.1% to 3.0%. In its latest World Economic Outlook, titled Global Economy at the Crosscurrents of War and Technology, the IMF highlighted a mixed global backdrop. While geopolitical tensions and higher energy costs are weighing on activity, strong demand linked to advances in artificial intelligence and broader technology adoption continues to provide an important counterbalance.

Looking further ahead, the IMF raised its forecast for global growth in 2027 from 3.2% to 3.4%, pointing to a moderate recovery following the slowdown expected in 2026.

Inflation, however, is likely to remain a challenge. Global headline inflation is projected to rise to 4.7% in 2026, up from 4.1% in 2025, before easing to 3.9% in 2027.

Despite the relatively resilient outlook, risks remain tilted to the downside. Further escalation in the Middle East could disrupt energy markets and weigh on growth, while rising trade fragmentation continues to threaten global supply chains and investment flows - take, for example, President Trump’s recent threat to halt all trade with Spain.

The IMF also warned that some of the optimism surrounding the technology sector may prove excessive. While AI is expected to support productivity and growth, uncertainty remains regarding the pace at which investment in the technology will translate into sustainable profits, and as competition intensifies and technology costs continue to decline, there is a risk that some of the growth expectations currently embedded in markets undergo reassessment.

Regionally, the IMF maintained its 2026 growth forecast for the United States at 2.3%, while lowering its forecast for the euro area from 1.1% to 0.9%. In contrast, China's growth projection was revised upward to 4.6%, from a previous estimate of 4.4%.

Weighing Eurozone inflation risks

Eurozone inflation has retreated from its recent peaks, supported by lower oil prices and easing price pressures across both goods and services. However, at 2.8%, inflation remains slightly above the ECB's 2% target, and recent developments suggest that the market's optimism may have been premature.

There are signs that underlying inflationary pressures remain present. Producer prices in the Eurozone rose by 5.9% year-on-year in May, up from 5.0% in April and above market expectations. As producer prices often feed through to consumer prices with a lag, this may indicate that disinflationary momentum is not yet firmly entrenched.

Indeed, ECB Chief Economist Philip Lane has cautioned that second-round effects have yet to fully materialise in the real economy. Wage growth is showing tentative signs of acceleration, while productivity growth remains weak.

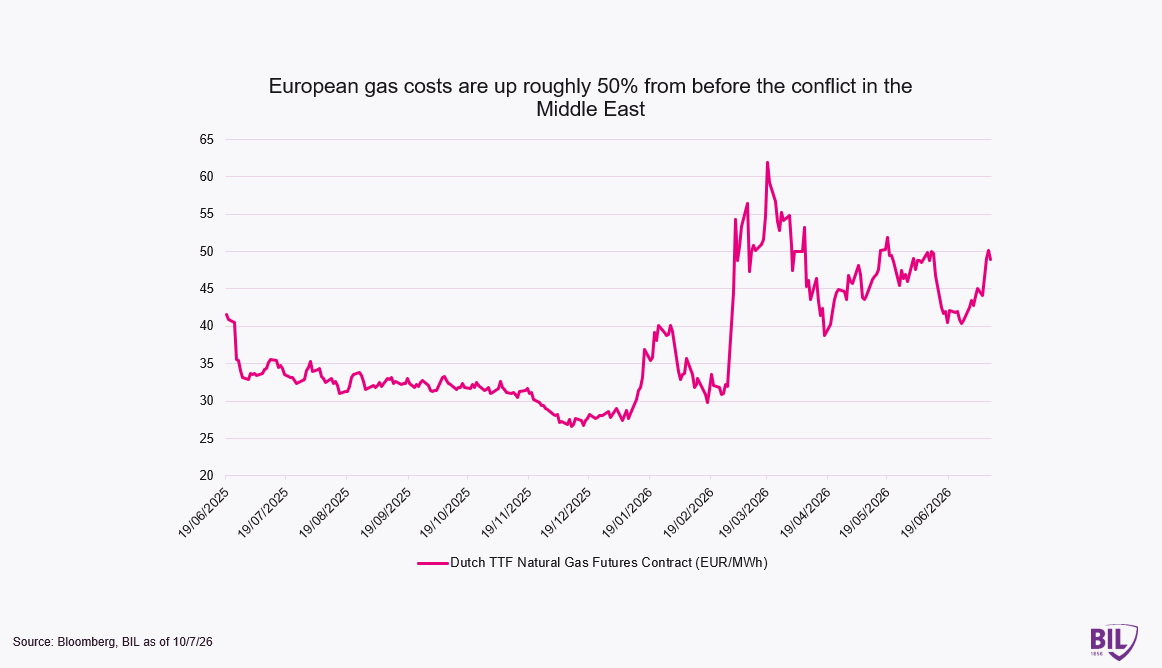

At the same time, recent developments in the Middle East have highlighted the vulnerability of global energy supply chains, keeping energy markets sensitive to further shocks and price volatility.

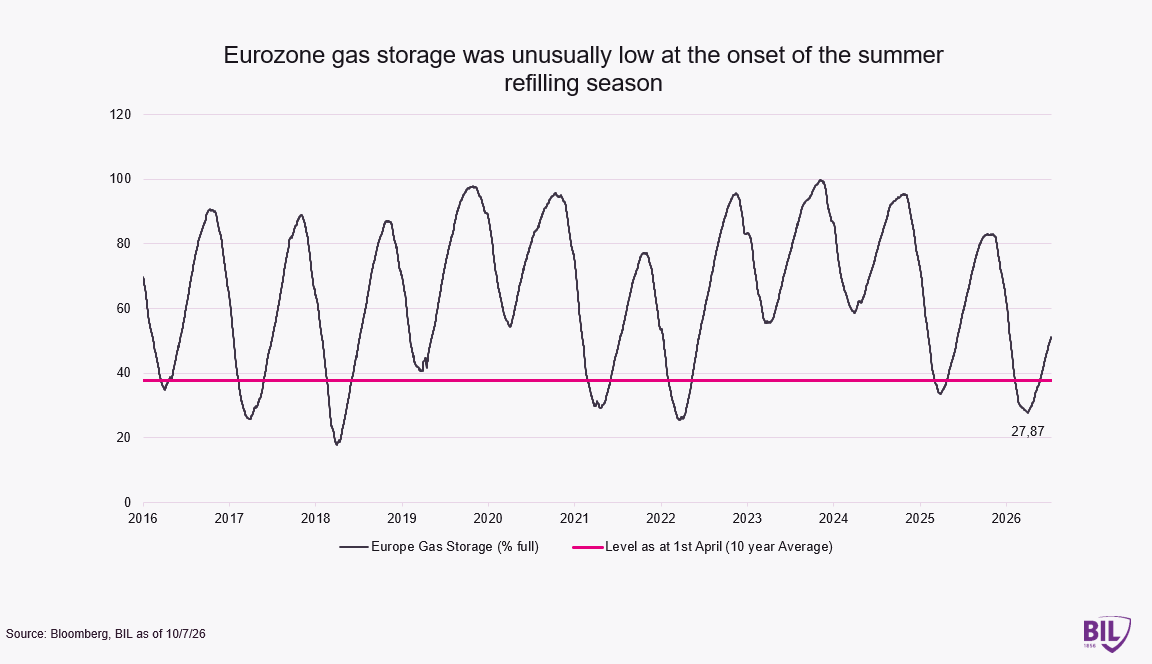

Europe faces an additional challenge closer to home. EU gas storage levels stood at just 28% at the start of the summer injection season on 1 April - the lowest level in four years and below the long-term average. Storage facilities will need to be refilled ahead of winter and while the EU's direct exposure to disruptions in the Strait of Hormuz is relatively limited, the region faces higher global energy prices and competition for LNG cargoes, particularly from Asia.

The bottom line is that inflation risks have not disappeared, they have merely shifted. While headline inflation has continued to recede, wage pressures, rising producer prices and ongoing energy-related uncertainties suggest the ECB may not be ready to declare victory just yet. As a result, the possibility of further policy tightening later this year cannot be entirely ruled out.

Eurozone retail sales rebound modestly in May

Eurozone retail sales volumes increased by 0.2% month-on-month in May, rebounding from a 0.3% decline in April. Growth was driven primarily by higher sales of food, beverages and tobacco (+0.6%), while sales of non-food products excluding fuel edged up by 0.1%.

In contrast, sales of automotive fuel declined for a second consecutive month (-0.5% following -3.6% in April), reflecting higher prices stemming from supply disruptions.

On an annual basis, retail sales volumes were 1.6% higher than a year earlier, suggesting that household consumption remains relatively resilient, despite ongoing economic uncertainty.

Calendar for the week ahead

Monday – OPEC Monthly Report

Tuesday – China Balance of Trade. US NFIB Business Optimism, Inflation (June), Fed Chair Warsh Testimony

Wednesday – China GDP Growth (Q2), Industrial Production, Retail Sales, Fixed Asset Investment. Eurozone Industrial Production. US PPI (June).

Thursday – UK GDP Growth(May), Industrial Production, Balance of Trade. US Weekly Jobless Claims, Retail Sales, NAHB Housing Market Index.

Friday – Eurozone Inflation (Final, June). US Housing Starts and Building Permits, Industrial Production, Michigan Consumer Sentiment (Preliminary, July).

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more