Research

March 7, 2024

NewsWeighing the impact of global warming on Europe’s winter economy

It’s peak ski season, but snow sport aficionados are arriving on European slopes to discover that a crucial ingredient is in short supply: snow. In the Alps, the world’s most popular ski destination, regions that depend on ski tourism are in a race against time to future-proof their business models.

The Alps are Europe’s most extensive mountain range and the world’s most popular snow sport destination. Attracting over 40% of global ski tourists each year, its snow sport industry is big business, with an estimated value of 30 billion euros. Local communities tend to be strongly dependent on the income from this spatially concentrated economic sector.

The risk of rising temperatures

Dwindling snowfall, however, means the industry’s future is increasingly uncertain. Temperatures in the Alps have risen by just under 2°C over the past 120 years - almost twice the global average. In some resorts, the effects of this are in plain sight, with skiers greeted by thin ribbons of snow on otherwise brown hillsides. The past twenty years have seen an average snow cover duration of just 215 days in the region – that’s 36 days fewer than the long-term average measured over the past six centuries. [1]

The risk is that warming becomes self-fulfilling: As areas covered with ice and snow (which reflect the sun’s rays) shrink, underlying rock and vegetation absorb the sun’s heat and contribute to even more melting.

As of now, the world is off-piste when it comes to the Paris Agreement’s goal of limiting global warming to well below 2°C above pre-industrial levels. The latest Emissions Gap Report from the UN Environment Programme finds we are on track for a 2.5-2.9°C rise this century.

A study of 2,234 ski resorts in 28 European countries [2] finds that 53% would risk running out of snow with global warming of 2°C. In this scenario, lower elevation resorts would be the most vulnerable. Those at higher elevations might survive but it is likely that they become increasingly unaffordable and exclusive. With warming of 4°C, the number of resorts at risk rises to 98%.

In a sign of the times, last year, the real estate company Savills’ rolled out a Ski Resilience Index. It ranks ski resorts on five factors: season length, altitude, temperature, snowfall and reliability (i.e., “the standard deviation of snowfall”). Resilience (usually found at higher altitudes) is increasingly important to buyers. We do not envisage a collapse in property prices, but a clear premium can be expected for real estate that is, at least for the near-term, immune to the impact of global warming.

Mitigation and adaptation

A lack of snow, decreasing snow depth and waning snow reliability could have a grave economic impact for winter tourism in the Alpine region. Faced with an existential crisis, the region’s ski resorts must pursue a combination of mitigation and adaptation strategies, striking a balance between business continuity and sustainability.

While ski resorts cannot combat global warming alone, mitigation involves doing what they can to minimize their own environmental footprint. For example, banning cars, encouraging public transport, and striving to use renewable energy wherever possible in resorts (for example, in hotels and to power ski lifts). To encourage sustainable travel, some stations now offer an “Alpine express pass” which gives discounts for snow passes, ski guides, and spas to people who travel to their holiday by train. There are, however, calls for a stronger industry-wide sustainability framework.

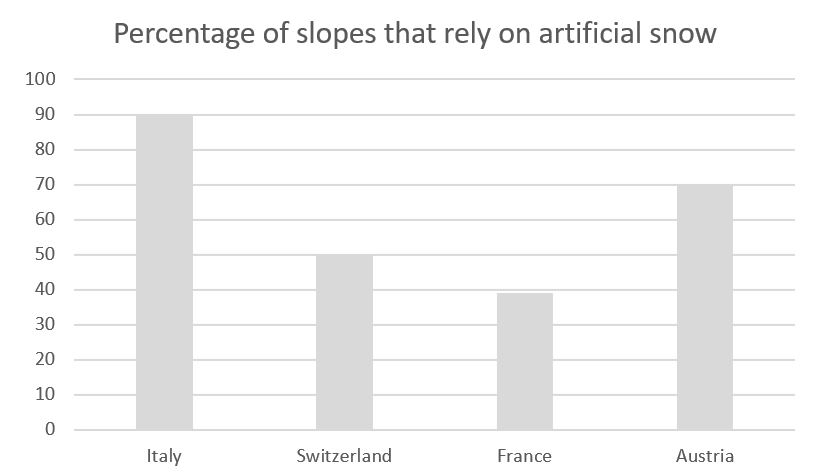

When it comes to adaptation, snowmaking is the most obvious example. This involves deploying artificial snow machines to “top up” areas where snow is too scant to ski upon. As seen in the chart, this method is widely used across Europe.

Source: Italian Green lobby Legambiente, Reuters, BIL

However, it is not a silver bullet. Firstly, it is expensive. Secondly, artificial snow can only be produced when temperatures stay below 1C, as the air has to be cold enough that the expelled water droplets freeze and turn into snow particles. This month, in Italy's Apennine Mountains it was simply too hot for snowmaking to be effective. Thirdly, artificial snow use at scale might detract from mitigation efforts given the amount of energy and water it entails.

In 2022, the Bank of Italy [3] wrote a report on climate change and winter tourism. It acknowledged that snowmaking might not be enough to sustain tourism flows, concluding that while man-made snow can reduce the financial losses from occasional instances of snow-deficient winters, it cannot protect against systemic long-term trends towards warmer winters. This led the bank to call for a more comprehensive approach to adaptation strategies. Resorts will increasingly need to diversify activities and revenues, for example, by promoting four-seasons tourism and investing in weather independent activities such as hiking and biking, as well as educational and health events.

A junction between passion, science, and economics

Recent ski conditions in Europe are a tangible reminder about the impact of climate change on our everyday lives. The ski industry finds itself at a junction where passion, science and economics collide, and if it fails to find a sustainable balance between the three, mountain regions might eventually have to contemplate life and business aprés ski.

To strike that balance, resorts are slaloming between adaptation and mitigation strategies, but some advocate that more formal governance of the industry is required.

References

[1] Carrer et al. (2023) “Recent waning snowpack in the Alps is unprecedented in the last six centuries”, Nature Climate Change, https://www.nature.com/articles/s41558-022-01575-3

[2] François, H. et al. (2023) Climate change exacerbates snow-water-energy challenges for European ski tourism, Nature Climate Change, https://www.nature.com/articles/s41558-023-01759-5

[3] https://www.bancaditalia.it/pubblicazioni/qef/2022-0743/index.html?com.dotmarketing.htmlpage.language=1&dotcache=refresh

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

BILBoard January 2025 – Snakes ...

While western New Year celebrations are already behind us, January 29th will usher in the Chinese New Year of the Snake. People belonging to that...

January 13, 2025

Weekly InsightsWeekly Investment Insights

Looking back on 2024, it was a year marked by conflict and political uncertainty, but it also saw major advances in space exploration, the...

January 10, 2025

NewsVideo summary of our Outlook 2025

2024 - The US economy exhibited impressive strength powered by consumption, while Europe struggled with weak demand and a protracted manufacturing downturn 2025 - The...

December 27, 2024

NewsBIL Investment Outlook 2025 – T...

Introduction from our Group Chief Investment Officer, Lionel De Broux As the oldest private bank in Luxembourg, we’ve been managing clients’...

December 20, 2024

Weekly InsightsWeekly Investment Insights

Having spent ten straight days decked out in red, the Dow Jones Industrial Average index recorded is longest losing streak since 1974. Other global...