BIL INVESTMENT INSIGHTS

The Copernicus Climate Change service reports that October 2023 was the warmest October on record. The same can be said for July, August, and September of this year; a year punctuated by a series of adverse weather events. With carbon emissions considered a key culprit in global warming, one might assume that the need for renewable energy has never been so great.

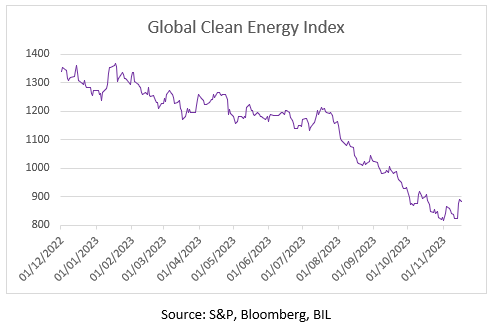

Yet, the sector that holds one of the keys to a greener future has found itself under intense pressure this year, with firms therein underperforming the broader market, as well as their fossil fuel peers. Year-to-date, the Global Clean Energy index is down by over 30%. The fall is even more surprising when one considers the multi-million-euro green stimulus packages disbursed by governments on both sides of the Atlantic.

The industry-wide downturn, which has affected all manner of players, from solar power companies to offshore wind developers, boils down to three major factors:

- Higher interest rates

- Inflation across the supply chain

- Barriers to price increases to allow firms to cover ballooning costs

Interest rates are a key area of sensitivity for the renewable energy sector because the projects usually require developers to borrow huge sums of capital up front to fund projects that span decades into the future. Expensive financing costs resulting from the “higher for longer” stance of major central banks, has rendered some projects altogether unviable. Ørsted, the largest offshore wind developer in the world, cited rising interest rates as a key reason why it recently decided to halt two offshore wind projects in New Jersey, resulting in impairments that could be as high as USD 5.6 billion.

While the cost of generating electricity from fossil fuels is largely driven by the price of the underlying commodity, the IEA estimates that a 5% rise in interest rates increases the levelized cost of producing electricity from wind and solar by a third.

And it isn’t only financing that has become more expensive. Prices across the supply chain were pushed up by pandemic-era bottlenecks and shortages and have yet to meaningfully subside. Swedish wind turbine developer Vattenfall this year said that its costs had climbed 40%.

For renewable power providers, the problem is that while costs have ballooned, the prices locked in for the power they generate have not. Owners typically sign long-term contracts to sell their electricity or secure subsidies before construction begins, so investors have a clear picture of future revenues and are less exposed to spot price gyrations. Many renewable projects were won back in 2019/20. Since then, the world has become very a different place.

Until now, we have seen pushback from authorities on requests to re-negotiate those contracts, sometimes compelling companies to cancel plans at a huge cost. BP noted the reluctance of state authorities to renegotiate terms as it wrote down USD 540 million on planned wind projects off New York. Also in the US, Spanish energy giant Iberdrola, cancelled an offshore wind project off the coast of Martha’s Vineyard, saying it was no longer possible at 2019 contract prices. Closer to home, Vattenfall halted work on its Norfolk Boreas project in the UK North Sea in July, again saying it was no longer viable at the electricity price it agreed with the government.

In sectors where companies are free to raise prices, they have their hands tied as consumers become more cost-conscious.

As an example, Enphase Energy, a maker of solar inverters, warned of below-estimate earnings on weak demand in the US, noting consumers are reining in spending due to high interest rates. This is akin to what we are seeing in the Electric Vehicle (EV) sector. Industry analysts say that the people who have held off buying an EV are likely price-sensitive shoppers, skeptical of making major adjustments to accommodate an entirely new technology. Convincing late adopters at this particular moment in time is a hard feat. As Elon Musk, Tesla CEO stated on the company’s Q3 earnings call, “A large number of people are living paycheck to paycheck, and with a lot of debt, they have got credit card debt, mortgage debt… We have to make our cars more affordable.”

Increasing competition from Chinese firms is another factor limiting strong price increases.

Looking Ahead

While it could take some time, we believe that the smog hanging over the renewable energy sector will clear. A lot of investors piled into green energy stocks, perhaps expecting immediate upside. However, as with all structural investment thematics, the idea is to benefit from a long-term societal shift. Rome was not built in a day and hiccups along the way are to be expected.

Already, the winds appear to be changing. The newest power projects are being struck at much better terms, which should allow companies in the sector to generate a profit moving forward, while supply chain disruptions are easing. At the same time, governments remain supportive – note the European Commission’s Wind Power Action program announced in October, which aims to significantly increase wind installed capacity and improve access to financing for companies. Moreover, we appear to have reached peak interest rates in both the US and Europe, with markets expecting cuts to begin in 2024.

The biggest support underpinning the renewable sector over the longer-term, however, is that fact that the need to decarbonise hasn’t gone away, even if it has been eclipsed by more immediate issues in the headlines. The COP28 in Dubai which kicks off on November 30th will probably give the topic more impetus.

Ultimately, we are reaching the beginning of the end for fossil fuels. The IEA predicts that demand for oil, natural gas and coal will all peak before 2030, creating huge growth potential for renewables. Just look at wind power – a key alternative favoured by governments. In 2022, it only accounted for 0.8% of global electricity output…

Disclaimer

All financial data and/or economic information released by this Publication (the “Publication”); (the “Data” or the “Financial data

and/or economic information”), are provided for information purposes only,

without warranty of any kind, including without limitation the warranties of merchantability, fitness for a particular

purpose or warranties and non-infringement of any patent, intellectual property or proprietary rights of any party, and

are not intended for trading purposes. Banque Internationale à Luxembourg SA (the “Bank”) does not guarantee expressly or

impliedly, the sequence, accuracy, adequacy, legality, completeness, reliability, usefulness or timeless of any Data.

All Financial data and/or economic information provided may be delayed or may contain errors or be incomplete.

This disclaimer applies to both isolated and aggregate uses of the Data. All Data is provided on an “as is” basis. None of

the Financial data and/or economic information contained on this Publication constitutes a solicitation, offer, opinion, or

recommendation, a guarantee of results, nor a solicitation by the Bank of an offer to buy or sell any security, products and

services mentioned into it or to make investments. Moreover, none of the Financial data and/or economic information contained on

this Publication provides legal, tax accounting, financial or investment advice or services regarding the profitability or

suitability of any security or investment. This Publication has not been prepared with the aim to take an investor’s particular investment objectives,

financial position or needs into account. It is up to the investor himself to consider whether the Data contained herein this

Publication is appropriate to his needs, financial position and objectives or to seek professional independent advice before making

an investment decision based upon the Data. No investment decision whatsoever may result from solely reading this document. In order

to read and understand the Financial data and/or economic information included in this document, you will need to have knowledge and

experience of financial markets. If this is not the case, please contact your relationship manager. This Publication is prepared by

the Bank and is based on data available to the public and upon information from sources believed to be reliable and accurate, taken from

stock exchanges and third parties. The Bank, including its parent,- subsidiary or affiliate entities, agents, directors, officers,

employees, representatives or suppliers, shall not, directly or indirectly, be liable, in any way, for any: inaccuracies or errors

in or omissions from the Financial data and/or economic information, including but not limited to financial data regardless of the

cause of such or for any investment decision made, action taken, or action not taken of whatever nature in reliance upon any Data

provided herein, nor for any loss or damage, direct or indirect, special or consequential, arising from any use of this Publication

or of its content. This Publication is only valid at the moment of its editing, unless otherwise specified. All Financial data and/or

economic information contained herein can also quickly become out-of- date. All Data is subject to change without notice and may not be

incorporated in any new version of this Publication. The Bank has no obligation to update this Publication upon the availability of new data,

the occurrence of new events and/or other evolutions. Before making an investment decision, the investor must read carefully the terms and

conditions of the documentation relating to the specific products or services. Past performance is no guarantee of future performance.

Products or services described in this Publication may not be available in all countries and may be subject to restrictions in some persons

or in some countries. No part of this Publication may be reproduced, distributed, modified, linked to or used for any public or commercial

purpose without the prior written consent of the Bank. In any case, all Financial data and/or economic information provided on this Publication

are not intended for use by, or distribution to, any person or entity in any jurisdiction or country where such use or distribution would be

contrary to law and/or regulation. If you have obtained this Publication from a source other than the Bank website, be aware that electronic

documentation can be altered subsequent to original distribution.

As economic conditions are subject to change, the information and opinions presented in this outlook are current only as of the date

indicated in the matrix or the publication date. This publication is based on data available to the public and upon information that is

considered as reliable. Even if particular attention has been paid to its content, no guarantee, warranty or representation is given to the

accuracy or completeness thereof. Banque Internationale à Luxembourg cannot be held liable or responsible with respect to the information

expressed herein. This document has been prepared only for information purposes and does not constitute an offer or invitation to make investments.

It is up to investors themselves to consider whether the information contained herein is appropriate to their needs and objectives or to seek advice

before making an investment decision based upon this information. Banque Internationale à Luxembourg accepts no liability whatsoever for any investment

decisions of whatever nature by the user of this publication, which are in any way based on this publication, nor for any loss or damage arising

from any use of this publication or its content. This publication, prepared by Banque Internationale à Luxembourg (BIL), may not be copied or

duplicated in any form whatsoever or redistributed without the prior written consent of BIL 69, route d’Esch ı L-2953 Luxembourg ı

RCS Luxembourg B-6307 ı Tel. +352 4590 6699 ı www.bil.com.

Read more

More

June 19, 2026

Weekly Investment Insights

Written as of 19 June. Please note that there will be no Weekly Newsletter on 29 June. At the first FOMC meeting under Chairman...

June 16, 2026

BILBoardBILBoard Mid-Year 2026 – In sea...

Sunday, 21 June marks the official start of summer here in the northern hemisphere. Yet, after an unseasonably warm spring, conditions have turned cooler and...

June 15, 2026

Weekly InsightsWeekly Investment Insights

Written as of 15 June, After a volatile week, major US equity indices ended higher on Friday, supported by growing optimism around a potential...

June 5, 2026

Weekly InsightsWeekly Investment Insights

Written as at 5 June 2026 The record-breaking streak among chipmakers paused on Thursday after the outlook from a prominent player cast some doubt...

June 1, 2026

Weekly InsightsWeekly Investment Insights

Written as of 1 June 2026 US stock indices recorded new highs last week with investor optimism around AI serving as the driving force....